It's been a little over a year since my first article on Sears Holdings Inc. (NASDAQ:SHLD) was published on Seeking Alpha, this article was widely read and as of today, has over 650 comments. I have consulted with several hedge funds and wealthy individual investors in the US and abroad explaining my thesis on SHLD.

In this new article, I will show irrefutable proof that SHLD is an even better investment at under $8 dollars than it was at $16.27 last year. I will focus more on the transformation occurring and show proof that Eddie Lampert is making all the right moves by investing heavily in Shop Your Way and the Sears Resinurance subsidiaries instead of traditional advertising and the physical retail stores.

Confidently Investing in Sears after such a large decline in stock price seems absurd to the average investor until you find the proper case study and make yourself familiar with:

- Warren Buffett's tenure as CEO of Retailer Diversified Retailing Company, Inc. from 1967-1978

- Warren Buffett's other mentor Gurdon W. Wattles

- Charlie Munger's Declining Business Strategy

In this article, I will show the similarities between what is occurring with Eddie Lampert and Sears Holdings and what occurred when Warren Buffett combined two dying retailers with a holding company structure from 1967-1978.

As a prerequisite, understanding the transformation of SHLD and perhaps parts of this article require a knowledge of: Strategic Inflection Points, lessons taught in books such as The Innovators Dilemma, by Clayton Christensen, The Outsiders by William N. Thorndike Jr., The Art of War by Sun Tzu, Competitive Advantage by Michael Porter, Only the Paranoid survive by Andrew Grove, The Long Tail and Free both by Chris Anderson, The Membership economy by Robbie Baxter and finally The Art of the Advantage by Kaihan Krippendorff.

Unfortunately, most of the above mentioned books are not on the desk of the average day trader or stock broker and/or hedge fund manager and that is why SHLD is so hard to understand.

I will do my best to simplify and summarize some of these complex strategies and concepts to give a better understanding of the of what is happening at SHLD and a better way to view and value the future of SHLD.

Summary of the First Article

The thesis of the first article was that Sears Holdings, Inc. is an incredible investment because it has a holding company structure, several bankruptcy remote entities, including valuable brands that can be licensed or sold (Kenmore, Craftsman and Diehard), valuable underlying real estate worth many multiples of the current stock price, that can be sold, leased or merged with a REIT, and a Re-insurance division, and Shop Your Way.

I cited several case study's such as the transformation of General Dynamics from 1991-1994, I showed the transformation of "dying retailers" with valuable underlying real estate such as Alexander's and Two Guys which eventually transformed into Vornado Realty Trust, a REIT with a market cap of 20 Billion.

The price of SHLD has gone down more than 50% since last year, and Investors like me, Force Capital, Bruce Berkowitz and Eddie Lampert are not insane or suffering from confirmation bias, the end game is not insolvency. To understand how to view an investment like SHLD we must first look at the affect that the strategic inflection point created by the internet has had on a Brick and mortar retailers like Macy's, Walmart, Sears and Kmart and others.

The Declining Business Strategy and the Six Competitive Forces

As discussed in Michael Porters book Competitive advantage and Andy Groves Book Only the paranoid survive, Businesses experience various types of competitive forces; the chart below is a diagram of these Six Competitive Forces taken from the book Only the Paranoid Survive by Andrew Grove

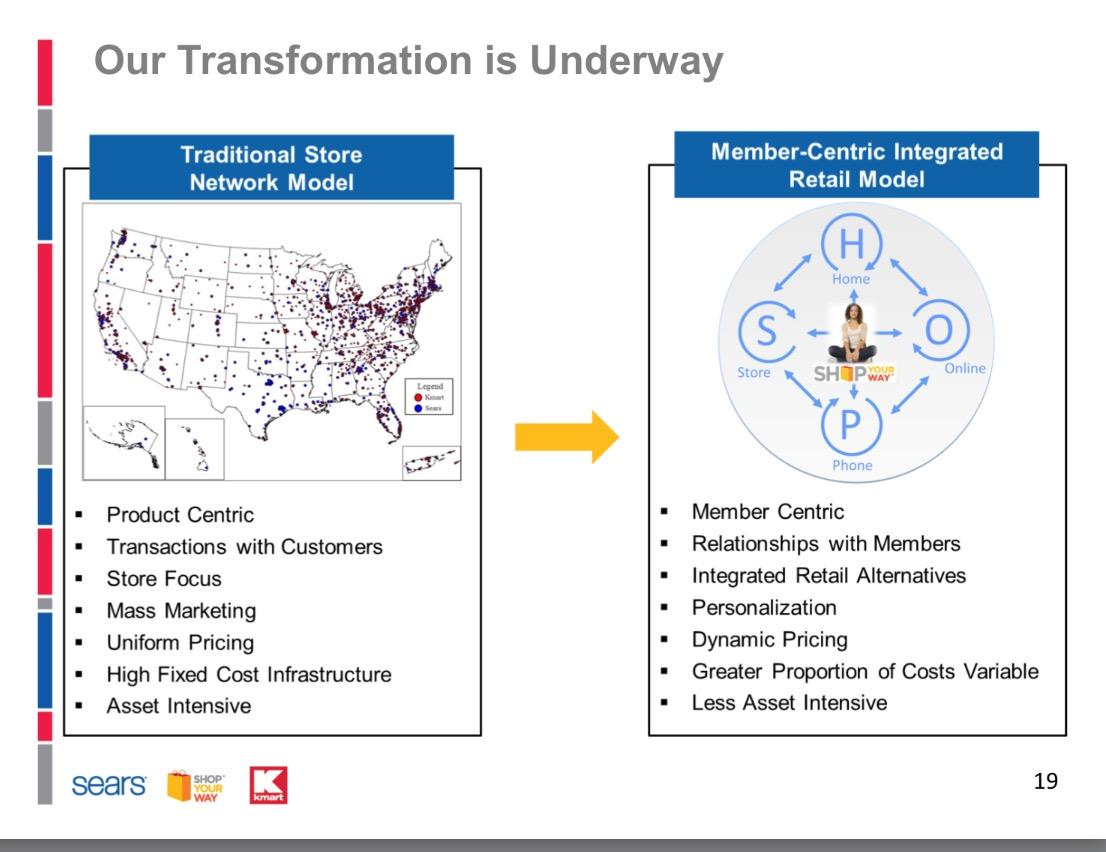

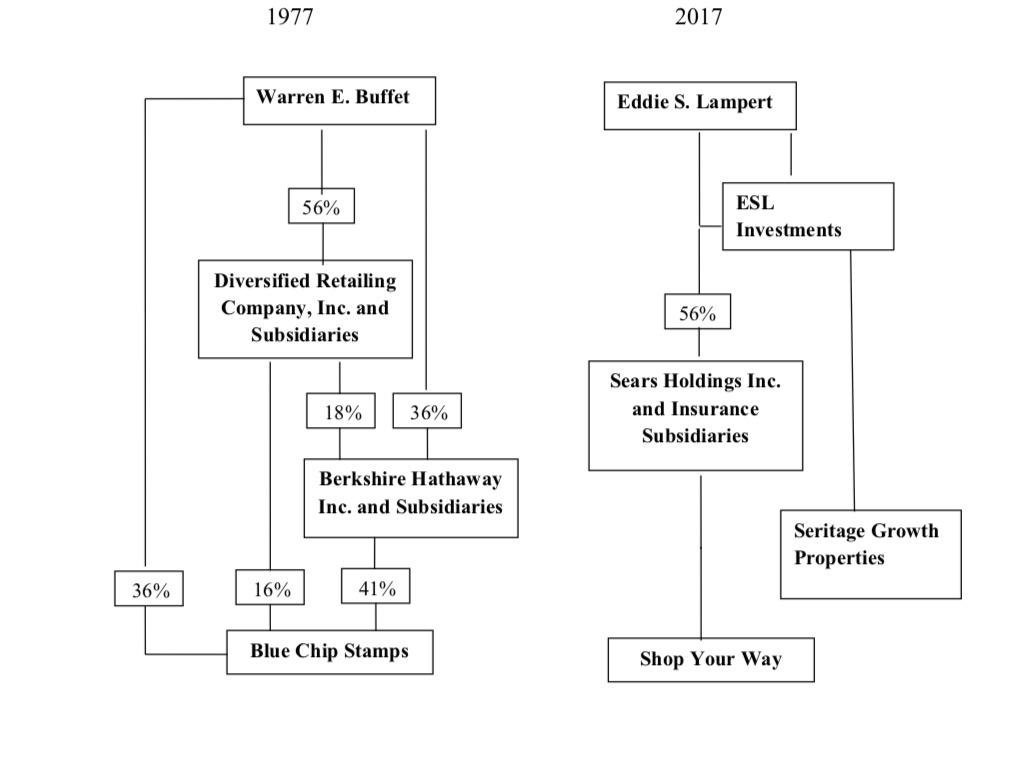

A 10X Factor occurs when a very large change is one of the Five competitive forces becomes ten times what it was recently, as shown in the chart below, this can occurs when there is a possibility that what your business is doing can be done in a different way. For example: In a nutshell, these above listed businesses and services cannot seek to turnaround their businesses, because the old way of doing business is not possible anymore, the customers have rapidly migrated to the new business model. Therefore these businesses must transform or die. A Turnaround is different than a transformation A turnaround is very different than a transformation, a turnaround is a caterpillar improving its ability to crawl, or crawl faster, a transformation is a caterpillar becoming a butterfly, once it transforms it can't go back to being a caterpillar, regardless of how well it used to crawl, that skill won't help the butterfly fly better or faster. When a company enters the market with a superior business model, the size and human resources of the old-line companies in some cases become a major liability, so reinvesting in what worked before (Turnaround) is a tremendous waste of resources. However, without hiring a consultant with strategic inflection point management experience such as myself or others, Billion dollar companies continue to attempt to compete based on the old business model, instead of transforming to the new business model (if possible) or investing heavily in the new business model, and/or others leading with the new business model For Example: Blockbuster should have invested heavily in Redbox and Netflix, record stores should have invested heavily in Apple (NASDAQ:AAPL), Borders Books should have invested heavily in Amazon.com. Investing in better taxi cabs or fixing up retail stores and/or spending more on traditional advertising doesn't change the fact that consumers want to purchase products and services in different ways, and in different places, they want cheaper faster more convenient transportation on demand a 'la Uber, they want to order from home and mobile a 'la Shop Your Way and Amazon.com, clearly a 10X factor has occurred, but Borders Books, Tower Records, Radio Shack, Sharper Image, Circuit City, Aeropostle, all attempted turnarounds instead of transformations and they all died. In a 2014 letter to Sears Alumni Eddie Lampert said: Turnarounds happen when a company succeeds again at doing what it had once done successfully before, transformations are almost entirely different-they occur when companies adapt their business model to fundamentals shifts in technology, competitive landscapes, government policies and regulations, or macro trends to serve their customers (or in our case, members) in new ways. Over the last decade Incidentally, Sears and Kmart have faced all the challenges I just listed" In the case of Blockbuster they were making 40% of there revenue on late fees so when Netflix launched their subscription service, promoting "no late fees" it was devastating to Blockbuster, but not obvious to them until it was to late. Netflix had no physical stores, very few employees and a larger selection of movies, eventually we became members of Netflix, when we were simply reluctant customers of Blockbuster. Record stores had customers but iTunes has members, via the iPhone or the actual service being provided, Amazon.com has members while most brick and mortar bookstores have customers, membership and analytics are the future of all commerce, traditional advertising without the use of analytics is a waste of a company's resources, targeted advertising is king now. Relationships have more value than transactions. When you build your business around a product anybody can steal your customer by offering a better, faster or cheaper product, but when you build your business model around the customer via membership you have essentially married the customer instead of just dated the customer. In the new economy you must marry the customer, this is done through membership, and the way to keep you keep them happy by anticipating their wants/needs, based on past purchases. Shop Your Way has millions of members, membership creates a marriage while a customer relationship is just a transaction similar to a blind date or a one nightstand at best. Navigating through a Strategic Inflection Point When one of the Five Competitive Forces sustains 10X factor businesses have several options: When a company is navigating through a strategic inflection point they are transforming from a caterpillar to a butterfly, as shown by this chart found in the book only the paranoid survive. Anyone who has read "Only the Paranoid survive" knows this chart and in fact those of us who are consultants use it as a template to demonstrate where the old business was and where it is going, the goal is to lead and to direct where it is going. The purpose of this chart is to show stockholders that you are fully aware of the 10X factor and are preparing for it, in this short video Eddie Lampert makes it clear that he is aware of the 10X factor caused buy the internet and he hinted that he may transform SHLD into a technology and information company. Mr. Lampert has a clear understanding of the 10X factor occurring to brick and mortar retailers, I believe Macy's (NYSE:M), J.C. Penney (NYSE:JCP), and Walmart (NYSE:WMT) are light years behind Sears Holdings, Inc. in this regard. This can be seen in how late these other companies were in closing down stores and creating a realistic online strategy. In this February 2013 Chairmans letter Eddie Lampert said: "As anybody can now see from the events surrounding J.C. Penney, Best Buy, and Toys "R" Us Staples, Barnes & Noble and others, the retail landscape is fundamentally shifting. In our case, observers have mistakenly concluded that our issues were primarily related to underinvestment in our stores. This ignores the significant investment that the retailers cited above and many others have made in their stores without relieving themselves of what I believe are the more fundamental issues facing the retail industry today. If it were just about store investment, then Best Buy would be thriving after the demise of Circuit City, Barnes & Noble would be thriving after the demise of Borders and other retailers who made significant investments would be thriving instead of struggling to chart a new course." Take a look at this chart below taken from the 3rd Quarter 2016 presentation. It looks just like the chart above in Andy Groves book. Note that the old business model is on the left and the new emerging business model on the right. In a nutshell Eddie Lampert gets it, he really gets it. I clearly understand the transformation occurring and know that drastic drops in stock price are expected with any company navigating through a strategic inflection point and transforming to an entirely different business model. The challenge is that most investors and the media judge a transformation by the same metrics as they would a turnaround, so when stores are closed the stock price usually goes down, when ESL loans the company money the stock goes down, but the numbers and metrics that mattered in the old business model are totally irrelevant in the era of the new business model. Shop Your Way is a Mini Amazon.com and Blue Chip Stamps 2.0 It is my theory that Eddie Lampert is successfully navigating Sears Holdings through a strategic inflection point by investing heavily in Shop Your Way which is a mini-amazon.com and an updated version of Warren Buffett's investment in blue chip stamps in the early 1970's. In this press release regarding Ivanka Trumps merchandise in Sears and Kmart Stores we discover that Shop Your Way is a mini-amazon.com with millions of products and thousands of sellers. The press release reads in part: Our Marketplace includes thousands of sellers offering millions of products to our members. Through this marketplace we are able to serve our members far beyond what we sell in our stores, including products and brands we do not purchase directly, in turn we offer our marketplace sellers access to tens of millions of shop your way members and our members have access to millions of products. Eddie Lampert is not dependent upon the old retail business model, he is investing heavily in Shop Your Way, at least eight hundred million in float exists from Shop Your Way's unredeemed points, for subscribers I have attached the last ten years of the unearned revenue of SHLD, note that in 2006 roughly 1.07 Billion in unearned revenue existed, today although hundreds of stores have closed, there is still roughly 800 Million in float as of January 2016. This revolving float can be used to invest in other securities or companies. Eddie Lampert is not only successfully navigating a strategic inflection point he is duplicating a strategy Warren Buffett implemented from 1967-1978 when he formed a holding company specifically to invest in retailers, this part of Warren Buffett's history is mostly unknown and misunderstood, he learned this strategy from Gurdon W. Wattles, Buffet explains this in his biography The Snowball on pages 387-389. For ten or fifteen years I followed him. He was Graham-like, very Graham-like. Nobody paid any attention to him except me. He was sort of my model of what I hoped to do for a while. It was so understandable and so obvious and such a sure way of making money. Although it didn't make you huge money necessarily, you knew you were going to make money. Case Study: Sears Holdings Inc, and Diversified Retailing Inc: Déjà vu all over again In 1966 Warren Buffet formed a Holding Company called Diversified Retailing Company, Inc. with Charlie Munger and Sandy Gottesman, this entity was formed for the specific purpose of owning retail companies. In 1967 DRC bought Associated Retail Stores, a chain of eighty stores based in NY, the same year they bought Hochschild-Kohn, a retail chain based in Baltimore, Maryland. Mr. Buffett justified his purchase of Hochschild-Kohn because the company had unrecorded real estate values and a LIFO inventory cushion, (sound familiar?) he went on to say that the retail chain had bad economics and he was lucky to break even, this was quoted in a book on Buffett by Carol Loomis found here. Buffett says they broke even but as explained later Charlie Munger mentioned how much they really made with these two "dying retailers" The first step was to set up a reinsurance business called Reinsurance of Nebraska (later renamed Columbia Insurance). In the 1973 Berkshire Hathaway letter discussing the potential merger between DRC, Inc. and BRK Mr. Buffet Said: Your Directors have approved the merger of Diversified Retailing Company, Inc., into Berkshire Hathaway Inc. on the terms involving the issuance of 195,000 shares of Berkshire, the net increase in the number of shares of Berkshire outstanding after the giving effect of the transaction will not exceed 85,449. Various regulatory approvals must be obtained before this merger can be completed, and proxy material will be submitted to you later this year so that you may voter upon it. Diversified Retailing Company, inc., through subsidiaries, operates a chain of popular-priced women's apparel stores and also conducts a reinsurance business, in the opinion of management, it's most important asset is 16% of the stock of blue chip stamps By year end 1973 DRC had amassed investments of nine million dollars, including stock in Blue chip stamps and 109,551 shares of Berkshire Hathaway, instead of investing in retail, the retail revenue was invested in insurance, other securities of other undervalued companies with float. Buffett and Munger successfully used the "declining business strategy" with their investment in DRC, and Blue Chip Stamps, the unearned revenue generated by unredeemed stamps and the float in the Reinsurance division, is listed as a liability on the balance sheet so an otherwise strong and healthy company can appear to have a significant liability that is called revolving float. Buffett and Munger eventually merged these DRC and Berkshire Hathaway in December 1978, he effectively bought the minority shareholders out with their own stock, as stated earlier this was a strategy Buffett learned from Gurdon W. Wattles. Mr. Wattles was later sued for effectively stealing the company he merged from the minority shareholders for far less than the book value, and not disclosing his control, the case is Mills v Electric Auto-lite, the oral argument before the Supreme Court can be heard here. To insure the minority owners didn't accuse Buffett of doing the same, when DRC merged with Berkshire Hathaway, Mr. Buffet did not participate in the merger negotiations and stipulated that he would consummate the merger only if the minority shareholders agreed. The merger was finally consummated on December 30,1978. Berkshire Hathaway issued roughly 195,000 shares for the 1,000,000 shares outstanding of DRC, but because DRC owned 178,000 shares of Berkshire the amount of shares actually issued were roughly 17,000. A look at the annual letters of Blue Chip Stamps from 1978-1982 show that they invested the income of the dying business in undervalued thriving businesses to off-set the losses of the declining business. They kept the name of the dying businesses (Blue Chip Stamps, Berkshire Hathaway) and while others sold their stock, Buffet and others kept buying. A look at this chart below shows the similarities between the two entities and the control Eddie Lampert and ESL has. His options are unlimited. Sears Holdings' Structure mirrors Warren Buffett' s Diversified Retailing Company, Inc. Shop Your Way has an identical business model to Blue Chip Stamps, the float in 1973 was roughly eighty million dollars, a huge sum of money at that time, the float created by unredeemed shop your way points is an astounding eight hundred million dollars, although Eddie Lampert has authority to do so, this money has not been invested yet and is more than the market cap of the entire company, For subscribers I have attached the pages of the balance sheets from 2006 to date that show the unearned revenue. The money from the dying retail divisions (Sears and Kmart) is being transferred to Sears Reinsurance through rental income on the 125 REMIC properties, license fees from KCD, LLP and extended warranty contracts, car insurance, worksman compensation, property and casualty insurance policies. All the 125 Properties are owned by Sears Re. On page six of the Q4 presentation, the Pension issues will be resolved by a 100M dollar real estate lien, and the income stream from future royalties generated by Craftsman. Conclusion The brick and mortar retail division may eventually fail or survive on a smaller scale, I believe the remaining real estate will be sold and/or merged with SRG. Shop Your way and Sears Reinsurance are the future. At a 2012 Berkshire Hathaway shareholder meeting when asked about investing in declining businesses Charlie Munger referenced his investment in Diversified Retailing Company, he said declining businesses are not worth as much as a growing business but they can be worth a lot if they are throwing off cash, Billions of dollars can come out of a declining business, we turned Six million into Thirty billion, all from a failed business, this can not be understated this is a return of 5000 times the investment. Eddie Lampert and Bruce Berkowitz are the Warren Buffett and Charlie Munger of our time, they have improved on their business model and long-term patient investors will be rewarded handsomely. Disclosure: I am/we are long SHLD, SRG, FAIRX, SHOS, LE. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source link

0 comments:

Post a Comment